[ad_1]

The global adoption of digital payments is increasing, and commercial payments are no exception.

During a recent PaymentsJournal webinar, Dean Leavitt, Founder and CEO of Boost Payment Solutions, and Steve Murphy, Director of Commercial Payments at Javelin Strategy & Research, discussed how corporates can modernize and transform operations, particularly commercial enterprise payments. They also highlighted four important strategic factors: cost mitigation, working capital, flexibility in rules implementation, and risk management.

Targeting these factors will help businesses keep abreast of trends in IT and help them focus resources in the face of economic instability.

Mitigating Hidden Costs in Payments Processing

Chief financial officers focus on cost control, but some costs are more obvious than others. “CFOs don’t necessarily focus on the cost of the cost, meaning what does it cost to make or receive a payment,” Leavitt said.

“According to data we collected, it can require 11 hours to manage a single invoice. And up to 15 people can be involved in managing that same single invoice. Roughly 3% of a business’ revenues are spent on managing B2B payments. So while the focus is appropriately on the cost of business items, there needs to be much more of a focus on the actual cost of making or receiving payments.”

In the B2B payments space, companies can mitigate costs by choosing payment methods that minimize transaction fees and exchange rate charges. To help optimize the acceptance of various payment methods, Leavitt suggests a list of questions companies should consider:

- Do you currently offer an early pay discount?

- What are your current payment terms?

- When are you actually getting paid?

- What are your labor costs to receive and process payments?

- If you’re accepting commercial cards as a form of payment, are you optimizing the way you’re receiving these payments?

Commercial credit cards can be highly advantageous for corporates, but they often induce negative reactions in the suppliers they pay. Suppliers typically bear the cost when accepting credit cards, so they have traditionally preferred direct deposit or ACH. When businesses ask some of the questions above and initiate a conversation with a supplier, it’s possible to reach creative and cost-effective solutions.

“Suppliers may be able to actually trade in, let’s say, a 2% early pay discount for card acceptance, to get paid at the same early timeframe at leass than a 2% discount,” Leavitt said. “So questions are obviously critical when you’re trying to develop a solution.”

Paying a fee for commercial credit card acceptance may cost less than the staff necessary to process a payment manually. “In the past year, we did some research on receivables, and about 75% of respondents—financial professionals and receivables folks—actually provide receivables or utilize receivables financing,” Murphy said. “When you consider card acceptance versus 75% doing receivables financing, it’s important to make sure that they know what they’re paying for because the cost of capital is going up.”

There’s also a broad misconception among financial professionals about the actual cost of accepting commercial cards, Leavitt said. “Historically, the costs might have been significantly higher,” he said. “But as the card networks have begun to address the needs of enterprise-level businesses, the cost of acceptance has come down significantly.”

Virtual Cards Can Improve Working Capital

In the B2B payments space, efficient payment processes can positively affect a company’s working capital by reducing the time between payment and receipt of funds. Central to increasing working capital is the use of virtual commercial cards.

According to Murphy, the use of virtual cards grew over the past five years and will continue to grow for good reason. Virtual commercial cards present a win-win. They can improve cash flow for buyers by increasing days payable outstanding (DPO), which is the number of days it takes to pay a supplier, and they improve cash flow for suppliers by reducing days sales outstanding (DSO), the number of days it takes to receive payment.

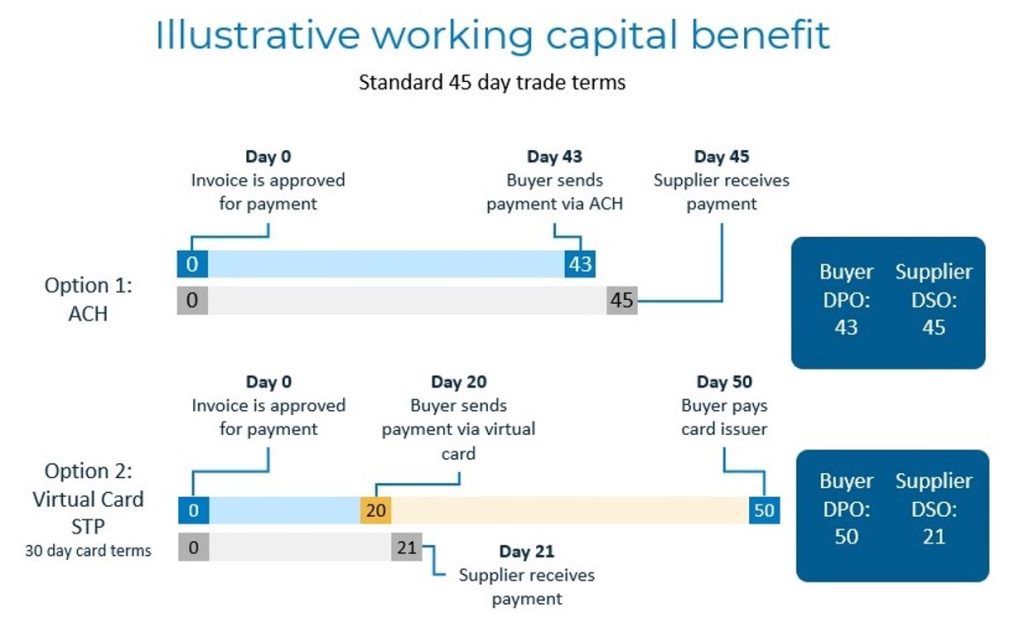

For a further breakdown, it helps to compare a virtual card payment to an ACH.

“Let’s say an ACH payment is due in 45 days,” Leavitt said. “The ACH is initiated on day 43, and the payee receives the funds on day 45. So you have a DPO of 43 days, and you have that 45 Day DSO.

“What we do is introduce a card product into the mix, to extend the grace period. If we reduce the payment date down to day 20, this reduces the DSO for the supplier from 45 down to 21. Because if you initiate the card transaction on day 20, the actual funds will be good and in the supplier’s account on day 21. But that initiates a grace period.”

“Assuming an end-of-month, plus-25-day cycle, you can extend your DPO out an additional five days from 45 to 50 days. So in this particular case, introducing card into the mix reduces the supplier’s DSO by 25 days and expands the DSO by five days for a true win-win scenario.”

Crafting a Data Strategy

The commercial payments industry is in the process of initiating payments and moving data from analog to digital. Although the payments infrastructure gets much of the press, the overall management of data is just as important.

“The No. 1 challenge when managing non-payroll spending relates to data errors,” Leavitt said. “This is because these processes are often HR-intensive and therefore introduce the possibility for error. Roughly 50% of businesses cite that data management costs are a key barrier to their ability to innovate. That’s incredible. Half the businesses out there have recognized this fact, and nearly half have reported receiving unusable information or remittance data.”

According to Murphy, poor data quality is responsible for part of the exorbitant cost of cross-border payments. “Missing data or incorrect data gets exacerbated in cross-border, because of different sovereign formats and regulations,” he said. “So it just multiplies cost by a factor of 1.5.”

Similar to sniffing out hidden costs in processing payments, the first step to improving data quality in corporate payments is asking the right questions and setting up a plan. This could also involve using a “data map” to get the right data to the right people, instead of having an employee do it manually. This map is a set of rules protocols, which are followed automatically by an IT system in assigning the right data correctly. “Most companies don’t have available to them significant resources right now to put towards operational efforts to change data flow,” Leavitt said.

Each industry has its own data-related particulars in the way it does payments, and it requires customized solutions. “There’s often a disparity between what a supplier or a buyer has in their respective accounting or ERP systems,” Leavitt said. “The version of the account number, it could be truncated or it could be just completely inaccurate because it’s less mission-critical for them to have the exact account number in their system versus the version that’s actually sitting on the biller’s system.

“In those cases, we’ll provide an account translation bridge to make sure that whatever payment is passed to that biller is received in their full and complete version of that account number. If you’re going to be digitizing their payment processes, you have to accommodate for those idiosyncrasies.”

Rampant Fraud Can Be Mitigated by the Right Payment Methods

Managing risk will be a top priority in 2023, particularly in reducing fraud.

“In 2021, nearly $2.5 billion was lost due to email-related compromises that resulted in a fraudulent payment,” Leavitt said. “And 75% of large corporations were victims of payment fraud and data hacks. Fraud is on the rise because the bad guys are getting better at what they do.”

Some kinds of payments are more susceptible to fraud than others, according to Leavitt. Checks, wire transfers, and ACH debits are considered high-risk, whereas virtual cards have the lowest level of fraud because their “straight-through” processing technology makes them inherently difficult to attack.

“With straight-through processing of virtual cards, neither the buyer nor the supplier receiving the payment have access to that card data,” Leavitt said. “It’s processed straight through without human intervention.” That’s what makes cards worth considering for CFOs focused on fraud reduction.

During the pandemic, companies were pushed to improve their digital operations, often partnering with fintechs like Boost. Fintechs can do not only things that corporates don’t have the resources for but also can develop new ideas and present possibilities to companies that financial institutions haven’t considered.

“A lot of what we do on a regular basis is educational,” Leavitt said. “It’s introducing enterprise-level buyers and suppliers to the tools that are available to them to expand working capital on both sides of the equation to reduce fraud and other types of risks associated with payments to introduce operational automation in ways that they didn’t previously envision, thereby reducing or allowing them to redeploy personnel in other more productive areas.

“The world has changed dramatically on so many different levels over the last couple of years. But as it relates to B2B payments, it’s an incredibly exciting time for both buyers and suppliers and those of us that serve them in the community of fintechs.”

[ad_2]

Source link